Abenomics: Why, What, and Now What?

Economic policies advocated by Japan prime-minister Shinzo Abe, since his return to the helm after the 2012 general elections, is referred to as Abenomics. This article aims to provide a first-level understanding of the principles of Abenomics and its effects on the global business environment.

Background

The Japanese economy was in a crisis situation for over 2 decades. As per commentators and analysts, the crisis initiated with the burst of Japanese asset bubble in 1991-92. What followed is commonly referred to as Ushinawareta Jūnen or the Lost Decade – a period of sluggish or no economic growth. In fact the “lost decade” was far longer than a decade. Some writers go to the extent of calling it “lost two decades”. The severity of the Lost Decade is, however, debatable. Nobel Laureate Economist Paul Krugman maintains that the story of Japan’s decline is an overstatement. His interpretation Japan’s slow economic growth was merely an effect of demographics (in this case Japan’s aging population leading to a dip in prospective workforce).

Japan was hit severely during the global economic recession in the 2008-09. In 2008, Japan suffered a real-GDP loss of 0.7% (global: 3.1% hike), while in 2009 the loss was a staggering 5.2% (global: 0.7% loss). Exports from Japan also dipped by 27% ($746.5B to $545.3B) from 2008 to 2009.

Japanese exporters faced tremendous challenge from Chinese and Korean competitors who were fast invading key Western markets.

Enter Abe

Shinzo Abe was first elected as prime minister in the 2006. His first stint was a short one, ending abruptly with his resignation in 2007. In September 2012 he was re-elected as the president of the Liberal Democratic Party. In December 2012 LDP aced the Lower House election, winning 294 seats out of 480.

Abe announced his return with the memorable words, “With the strength of my entire cabinet, I will implement bold monetary policy, flexible fiscal policy, and a growth strategy that encourages private investment, and with these three policy pillars, achieve results.”

Thus began Abenomics.

Challenges Abe faced

Abe’s key economic challenges at the time of his re-election were beating deflation, correcting a strong Yen, and achieving economic growth. Before proceeding on to the core of Abenomics, let’s first evaluate these challenges individually.

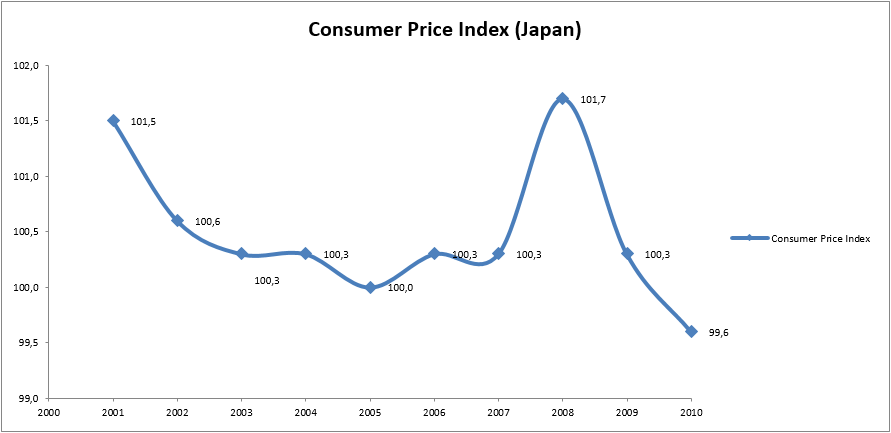

1. Beating Deflation In economics, deflation is a decrease in the general price level of goods and services. In Japan the deflation situation in the decade preceding the end of 2010 is captured well in the diagram below.

Deflation leads to problems both on the demand side as well as the supply side. Demand falls because customers defer purchases, anticipating a price fall in the future. Moreover, deflation increases the real burden of debt on debtors. On the supply side, deflation causes revenue drop for firms (due to price cuts), which leads to wage reduction for employees and increased unemployment.

2. Correcting strong yen The yen strengthened over time, from an exchange rate of 1USD = 120 JPY in 2007 to 1USD = 77JPY in 2012. Due to this strengthening, Japanese exporters faced a tough situation as Japanese goods got more expensive in the global market. The price challenge from Chinese and South Korean competitors further worsened this situation. The strengthening of the yen also led to lowering of foreign direct investment (FDI) in Japan.

3. Economic growth As already mentioned, since the beginning of the lost decade GDP growth in Japan has struggled: by 2013 the Nominal GDP in Japan was almost at the same level as that in 1991.

As a result of these challenges, Japanese firms faced tremendous difficulty to survive in business. Due to deflation, domestic-focused firms lost revenue. To make things worse, the exports were also not going well due to the strengthening of the yen. This combination led to job-cuts and unemployment. This, in turn, further depressed consumption levels and led the economy to a vicious cycle of depression.

Abenomics responds to the situation with a three-pronged approach (popularly called “the three arrows”)

- Monetary policies

- Fiscal policies

- Structural policies

The three arrows

To begin with we need to take note of the monetary policies. As a first step, BOJ (Bank of Japan) announced an inflation target of 2% (Abe had spoken about curbing their independence if they did not act). The method adopted for achieving the same was quantitative easing. In simple words, BOJ would increase (double) Japan’s monetary base and also buy more (twice as many) Japanese government bonds. As a result it is expected that the money that the banks get by selling off bonds would be used to loan money to borrowers. With this easing of difficulty in getting loans, consumers and businesses would both have more money at disposal and thus spending (consumption) would increase, leading to inflation. With inflation the businesses would make more revenue and hence it would lead to decreased joblessness and increased salary.

BOJ’s quantitative easing would solve two key challenges:

1. Beating deflation

2. Weakening the JPY (or rather correcting the strengthening yen)

As a part of the second arrow (fiscal policies), the Japanese government announced a hefty 10.3 trillion yen short-term stimulus package (cleared by cabinet in January 2013) for infrastructure projects. The intent behind this was to increase revenue for businesses and to allow for job creation. In October 2013 Abe also announced an increase in consumption tax from 5% to 8% to boost government earnings.

The third arrow (structural policies) remains the missing piece in the plan. This requires not just overhaul of regulations in key sectors but also a plan to overcome the growth-hampering effect of the troubled Japan demographics (aging population and decline in workforce). While the first two arrows are relatively easy to implement, structural policies are not. Especially because it leads to contradictions in message. Let’s consider a hypothetical example: If structural reforms demand deregulation in an industry and the government implements it then it will end up contradicting itself if it starts recommending pay hikes/employment in that industry (which again is a critical requirement for the success of monetary policies).

The Abe effect

The effects of the monetary policies were visible quickly after they were implemented. The yen weakened by over 20%, and in a couple of quarters the exchange rate had shifted to 1USD = >100JPY. The yen weakening provided relief to a whole bunch of Japanese companies who earned a significant portion of revenues through exports. A case in point would be Renesas Electronics. Renesas was almost headed toward bankruptcy when Abe took over. Renesas first began making operating profit and in the recently concluded fiscal quarter (Q3 2014 for Renesas) have managed to make 23 billion yen net profit. Those who follow the global semiconductor industry will attribute Renesas’s turnaround to a whole host of factors such as organizational changes, opex reduction, et cetera. One point however needs to be noted:

In Q3 2013 Renesas’s revenue was 191B yen and in Q3 2014 their revenue was 215.6B yen. In percentage terms, this translates to 13% growth YoY. If we evaluate the same numbers in USD instead of JPY, however, we note that there has actually been a revenue decline of 10%.

Renesas was not the only company to report advantage due to Abenomics. The Bank of Japan Tankan survey of business sentiment showed business sentiment rising to a six-year high. Riding the positive recovery story of these companies, Nikkei stock exchange made an annual gain of 57% in 2013—its biggest gain in 42 years.

Japan’s core consumer prices (excluding non-volatile food prices) recorded the biggest annual rise in five years (0.8% increase between August 2012 and August 2013).

However, on the flip side, Abe’s vision that companies would pass on the additional profits to employees in form of salary hikes (such that the salaried Japanese individuals don’t feel the pinch of inflation) has so far fallen short of expectations. A recent survey by Reuters revealed that only 11% of Japanese companies plan to increase employees’ total compensation (base pay plus bonus). 66% of companies expressed intent to increase only the bonus component. Though prices have gone up by 1.3% year-over-year, the increase in salaries is 0.8%. The reluctance among firms to increase salaries could possibly be dangerous for Abenomics, as it would restrict consumption increase by the masses (only 2.4% increase in private consumption).

Further, while companies are investing, the current rate of 1.3% rise in capital investment falls short of typical expectations from a recovering economy.

It is impossible for government to control the spending patterns of firms without contradicting itself given its structural reforms, the third arrow of Abenomics, are aimed at relaxing fiscal controls, loosening the labor market, and making it easy for a business to start and operate in Japan. Akira Amari, the minister of state for Economic Revitalization, had remarked (earlier in 2013), “I want to create an environment where it’s embarrassing for a company not to raise wages.” In fact, the actual government response to the situation was linking corporate tax structure to salary increases. The response no doubt is fair, but is contradictory to the initial promises.

Global business impact and forward outlook

The global impact can be judged by the mixed global reactions thus far. Abenomics has found support from countries who intend to increase FDI in Japan. On the other hand, countries whose key export areas are same as those of Japan have expressed concerns about the potential damage to their export businesses.

Hyun Oh-Seok, finance minister of South Korea, commented “We need some kind of coordinated efforts to prevent these kinds of unintended side effects from [Japan’s new] monetary policy. Whether it is intended or not, the result [of the depreciation of the Japanese yen] is quite quick.” South Korea’s top 10 exports compete directly with Japan. Another country facing similar concerns is Germany.

Companies that export to Japan (and have Japanese competitors) have reported feeling the pinch of Abenomics. This is because these companies in quite a few cases could not increase prices in yen to their customers. Instead they had to lower the prices in their own accounting currency.

On the other hand, the has been a sharp increase in the prices of commodities imported by Japan. In fact, the increase in money spent for importing has beaten the incremental money earned through increased exports. This has resulted in record trade deficits for Japan. This, in turn, is making the world question Japan’s long-term economic recovery prognosis. Credit Suisse AG has cut their Japan growth forecasts (Feb 2014) for the year 2014 from 2.2% to 1.6%.

References

- http://japandailypress.com/japanese-companies-reluctant-to-increase-base-wages-says-reuters-survey-2144691/

- http://www.foxnews.com/world/2013/07/02/japan-salarymen-still-feel-pinch-despite-abenomics/

- http://finance.yahoo.com/news/japans-economy-grows-slower-pace-033138096.html

- http://www.zerohedge.com/news/2013-06-02/south-korea-demands-international-action-against-negative-impact-abenomics

- http://www.businessweek.com/news/2014-02-20/japan-s-record-trade-deficit-shows-risks-mounting-for-abenomics

- http://blogs.reuters.com/james-saft/2014/02/18/column-abenomics-wobbly-arrows-james-saft/

1 Comments

About The Author

brilliant stuff anirban. Very well compiled!